Wednesday, 11 October 2023

Balancing Debt and Savings: A Practical Guide to Financial Wellness

Achieving financial wellness involves managing your debt responsibly while also saving for your future. Balancing these two aspects of your financial life can be challenging, but it’s a crucial step towards achieving your long-term financial goals. In this article, we’ll provide valuable advice on how to strike the right balance between debt repayment and savings.

The Importance of Balancing Debt and Savings

Before diving into the tips, let’s understand why finding this balance is so important.

1. Emergency Preparedness: Savings act as a safety net in case of unexpected expenses like medical bills or car repairs. Without savings, you might turn to more debt to cover these costs.

2. Long-Term Financial Goals: Saving for goals like homeownership, education, or retirement requires disciplined savings. Relying solely on credit can lead to higher costs in the long run.

3. Financial Stability: A balanced approach helps improve your financial stability. It can reduce financial stress and improve your overall well-being.

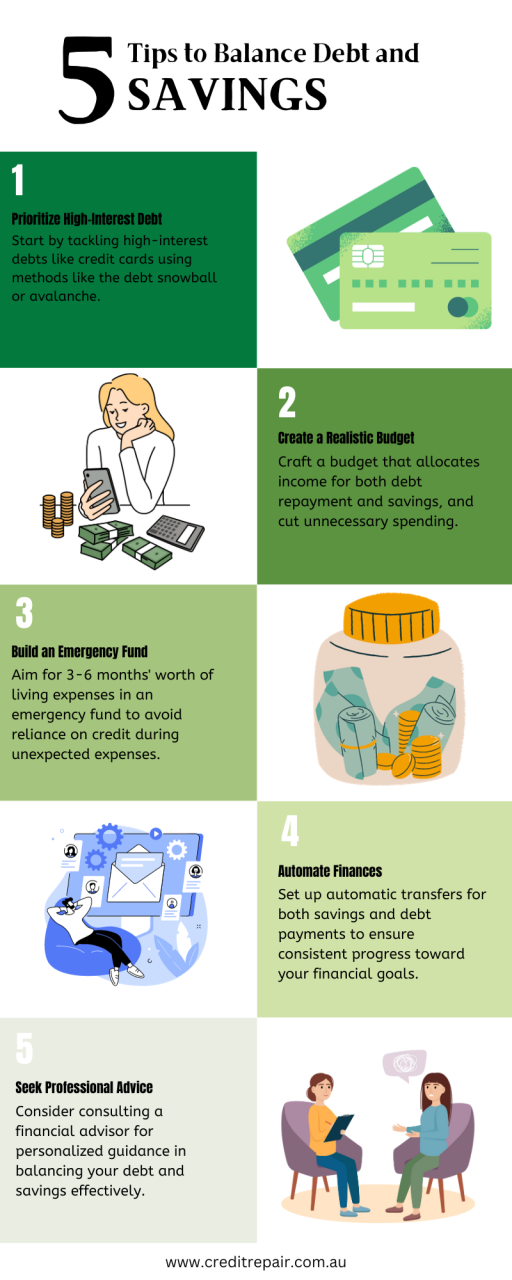

- Â Tip 1: Prioritize High-Interest Debt

Begin by focusing on high-interest debts like credit card balances or payday loans. These types of debt accrue interest quickly and can become overwhelming if left unchecked. Here’s how to tackle them:

-Â Snowball or Avalanche Method: Consider using either the debt snowball method (paying off the smallest debts first) or the debt avalanche method (paying off the highest interest rate debts first). Choose the strategy that suits your psychology and budget.

-Â Consolidation: Look into debt consolidation options, like a personal loan or a balance transfer credit card with a 0% introductory rate. This can help lower interest costs and simplify your debt repayment.

- Tip 2: Create a Realistic Budget

To balance debt repayment and savings effectively, you need a budget. A well-crafted budget ensures you’re allocating your income efficiently. Here’s how to do it:

-Â Track Your Expenses: Start by tracking all your expenses for a month. This will give you a clear picture of where your money is going.

-Â Set Priorities:Â Allocate a portion of your income to both debt repayment and savings. Make it a non-negotiable part of your budget.

-Â Cut Unnecessary Spending: Identify areas where you can cut back on discretionary spending. The money saved can be redirected towards debt and savings.

- Tip 3: Build an Emergency Fund

While paying down debt is crucial, don’t neglect your emergency fund. Having savings for unexpected expenses prevents you from relying on credit cards or loans when emergencies strike. Aim for at least three to six months’ worth of living expenses in your emergency fund.

- Â Tip 4: Automate Your Savings and Debt Payments

Make your financial life easier by setting up automatic transfers for both savings and debt payments. This ensures that you consistently contribute to your financial goals without having to remember to do so manually.

- Tip 5: Seek Professional Guidance

If you’re struggling to find the right balance between debt and savings, consider consulting a financial advisor. They can provide personalized advice based on your unique financial situation and goals.

Balancing debt and savings are a critical aspect of achieving financial wellness. By prioritizing high-interest debt, creating a realistic budget, building an emergency fund, automating your finances, and seeking professional guidance, when necessary, you can navigate this financial juggling act successfully. Remember that it’s not about eliminating debt or saving everything, but about finding a sustainable equilibrium that aligns with your financial objectives and peace of mind.

since version 3.0.0 with no alternative available. Please include a comments.php template in your theme. in

You're an Australian resident

You're an Australian resident

Leave a Reply