Wednesday, 11 January 2023

5 causes of insolvency & how to avoid them

Many factors can lead to mounting debts that put an individual at risk of insolvency. While some of them, such as unexpected job loss or illness, can be outside your control, there are measures you can take proactively to protect yourself. Here are the five biggest causes of individual insolvency in Australia and tips for what you can do to avoid or better manage them.

1. Excessive use of credit

Recent data from the Australian Financial Security Authority (AFSA) revealed that excessive credit use has now overtaken unemployment as the leading cause of personal insolvency. The AFSA report cites common reasons for excessive credit use as including losses on repossessions, high interest repayments and financial pressure. Ways to reduce your reliance on credit include:

- charge only what you can afford

- never miss a credit card payment

- pay your balance in full each month whenever possible

- don’t get cash advances on your credit card

- avoid balance transfers

- limit the number of credit cards you have

2. Unemployment or loss of income

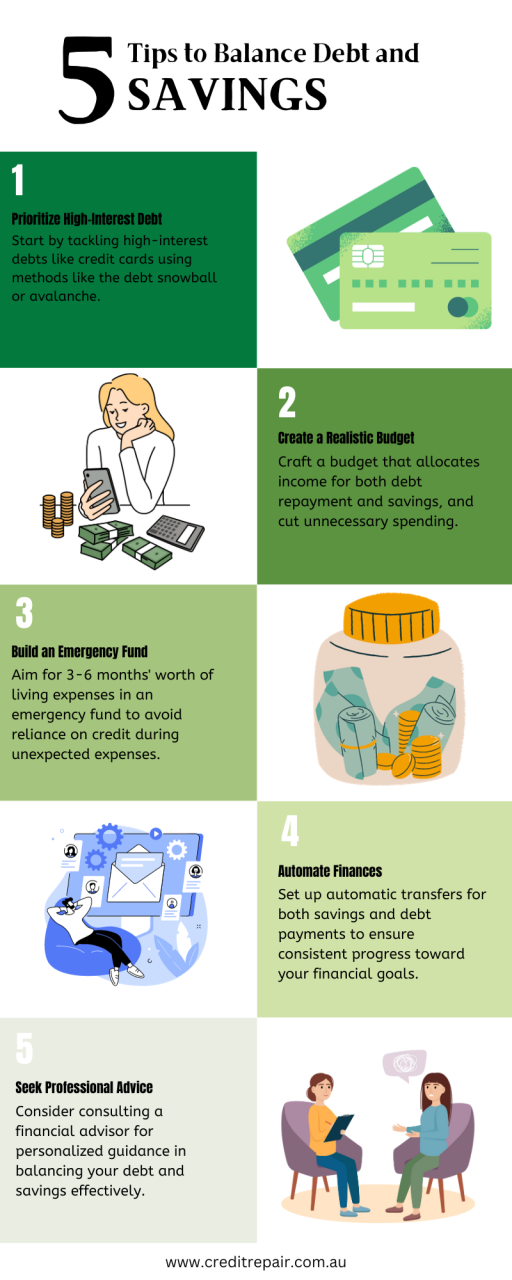

Unsurprisingly, unexpected unemployment or loss of income is another major factor in people becoming insolvent. The best way to protect yourself is to build up an emergency savings fund that would cover all of your living expenses for at least three to six months in the event of unemployment. Depending upon your line of work and individual circumstances, it may also be worth taking out income protection insurance, which can help protect you and your family if you are unable to work.

3. Relationship breakdown

It’s a sad reality that many Australian marriages end in divorce. Aside from the emotional consequences, divorce can lead to devastating financial fallout. There’s rarely a single cause, but if you were already over-stretched, divorce can push financial woes over the edge. A divorce can mean splitting up assets and suddenly living on one income rather than two, as well as increased costs. Doing whatever you can to protect your individual and joint assets in advance is critical, as is getting good professional advice. ASIC’s MoneySmart offers this helpful guide to financially managing divorce and separation.

4. Ill health

An illness that leaves you unable to work for an extended period can also wreak havoc with your finances and put you at risk of insolvency if you can’t cover your debts during this time. This is another time when it pays to have at least three to six months of living expenses stashed away safely. Being adequately insured, including having health insurance that will minimise your costs during an illness, is also important.

5. Gambling

Ironically, those on the brink of bankruptcy spend more on gambling, according to the Salvation Army. Presumably, this is often in an attempt to lift oneself out of a financial sinkhole, but it rarely works and gambling is also one of the major causes of personal insolvency. Research by the Australian Gambling Research Centre (AGRC) shows that a significant number of gamblers bet more than they can afford to lose. There are many ways to find help before a potential problem spirals out of control.

If you’re struggling with debt, visit our website to read more about our debt solutions or contact us to find out how we may be able to help you.

since version 3.0.0 with no alternative available. Please include a comments.php template in your theme. in

You're an Australian resident

You're an Australian resident

Leave a Reply