Tuesday, 28 March 2023

How can shopping hurt your credit score?

We all love a little retail therapy. Not to mention, shopping is often essential as well as pleasurable. However, shopping can be harmful to your credit history in ways you may not even have considered. This can have a knock-on negative effect on important life decisions, such as getting a home loan or car loan or applying for a new job.

Data mining and credit cards

Besides the financial risks of living beyond your means if you’re shopping too much, what you purchase may lead you to be seen as a poor credit risk to lenders.

Credit card companies compile data from thousands of transactions. As a result, they have sophisticated algorithms that automatically detect certain patterns. These can alert them to certain customer spending patterns that are known to be correlated with behaviours that indicate a credit risk, such as missed or late payments or a high debt to credit ratio, but also certain types of purchases.

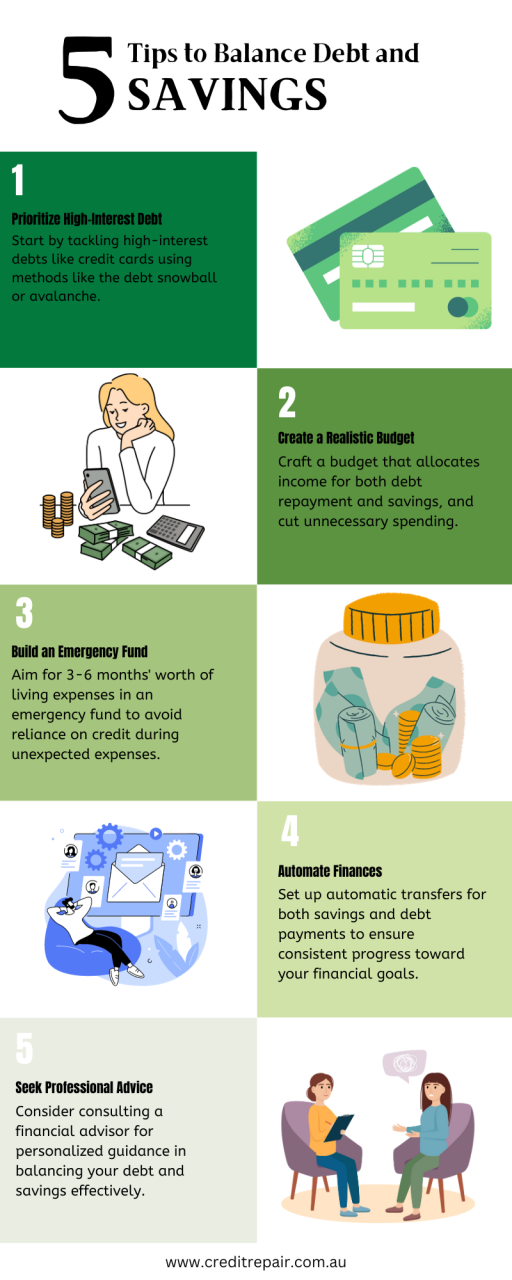

Start managing your credit card debt today.

Risky purchases?

Some examples of regular purchases on your credit card that could act as red flags, include:

Traffic fines — Paying for your excessive traffic fines or court fees on your credit card can be seen by lenders as a sign you are at risk of defaulting on your payments.

Lottery tickets — Because lottery tickets are historically purchased in greater quantities by people in lower socioeconomic groups (e.g. those with less money), regularly buying them can be another sign you’re in need.

Income taxes — Although the tax department is perfectly fine with you paying your taxes by credit card, your lender may not be. A credit card company may see this as a sign that you can’t meet your basic financial responsibilities.

Alcohol — If you are making excessive purchases of alcohol (in stores or at bars) on your credit card, this can also be viewed as a warning sign of bigger life problems.

Cash advances — Never get a cash advance on your credit card to shop. In addition to paying higher rates on repayment, it is a red flag to lenders that you’re struggling financially.

How to protect yourself

If any of the above spending patterns apply to you – or particularly if several do – consider paying cash only for these transactions or getting help to better manage your finances ongoing.

Credit cards and overspending

Another way that shopping can harm your credit history is if you are living beyond your means. If this leads to you only being able to pay the minimum on your credit card or, worse, having late or missed payments, then this can also result in black marks on your credit report.

Make sure that you’re budgeting properly and keeping your spending to what you can actually afford. Many people find that only using cash for discretionary shopping, as opposed to necessities such as food or petrol, helps them keep costs under control.

To learn more about what’s in your credit history, get a free copy of your credit report.

since version 3.0.0 with no alternative available. Please include a comments.php template in your theme. in

You're an Australian resident

You're an Australian resident

Leave a Reply