Tuesday, 2 August 2022

3 options for dealing with unmanaged debt

When debts pile up and become unmanageable it can be overwhelming. However, there are options you can – and should – explore for getting on top of the situation.

1. Negotiating a repayment plan with your debt collectors

If you are struggling to repay a debt that is yours, you may be able to negotiate a repayment plan with debt collectors. In some cases a debt collector may agree to extend your repayment period or allow you to make smaller repayments over a longer time. ASIC’s MoneySmart provides more information on this option.

2. Get professional help

A financial counsellor or professional debt solutions company will discuss your options with you, help you with budgeting, refer you to other sources of assistance and even speak to creditors on your behalf.

3. Consider the debt solutions available to youÂ

There are a number of debt solutions that can help you resolve the unmanaged debt. These include both formal and informal solutions. Informal solutions can be easier to start, stop and adapt, whereas formal debt solutions are often set in stone and may be legally binding.

Informal debt solutions include:

Debt consolidation loans involve rolling all your existing debts into one loan. This allows you to make multiple payments, which may make it easier to budget and may have a lower interest rate. However, you could also end up paying more over the life of the loan depending on the interest rate and loan terms.

A debt settlement is when you make an offer to your creditors that is less than the full amount you owe to wipe out your debt. You may be able to settle your debt for less than the full amount.

Formal debt solutions include:

Debt agreements allow you to make regular repayments to repay your debt and may let you pay back less than what you owe. Whilst a debt agreement is an alternative to bankruptcy, submitting a debt agreement proposal is still classified as an “Act of Bankruptcyâ€. If the proposal is not accepted by creditors, a creditor can use this to apply to the court to make you bankrupt.

Personal insolvency agreements are arrangements between you and your creditors to pay an agreed amount in instalments. These are usually reserved for people who have over $100,000 worth of debt. This is considered an act of bankruptcy and may affect your credit score.

Declaring bankruptcy should be seen as a last resort as it is a serious step that will affect your credit for a long period, as well as your ability to travel overseas and get some types of employment. However, at the end of the bankruptcy period (3 years and 1 day) you will be released from your debts.

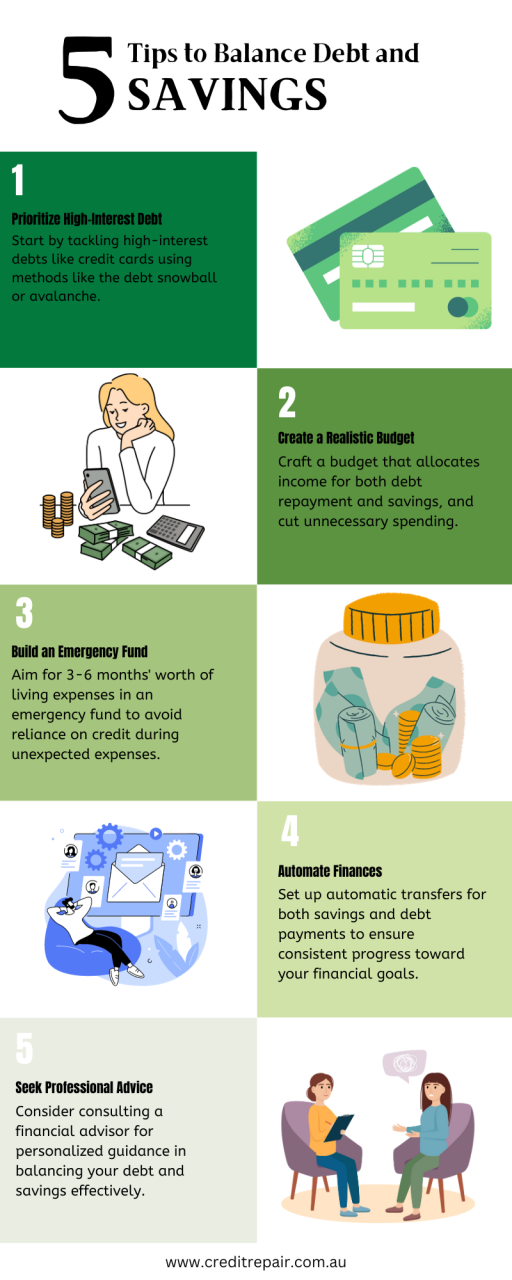

Tips for managing debt ongoing

• Make a realistic and sustainable budget. It’s possible to budget on a low income.

• Manage your credit to prevent future issues occurring.

• Be aware of types of shopping that can affect your credit score.

• Practice good habits that improve your credit rating.

If you are struggling to manage your debts, an expert debt solutions company like Credit Repair Australia can help. Find out more about our debt solutions.

since version 3.0.0 with no alternative available. Please include a comments.php template in your theme. in

You're an Australian resident

You're an Australian resident

Leave a Reply